If you have experienced a financial hardship and you are struggling to make your monthly mortgage payment and need to STOP A FORECLOSURE IN UTAH or across the country, we can help you!!! We understand that defaulting on a mortgage is a very emotional and stressful situation. We are foreclosure and short sale experts that have assisted many individuals and families that are in the same situation. Our team of real estate professionals, tax consultants, real estate and bankruptcy attorneys, and credit repair specialists can help you prevent or stop foreclosure, negotiate a short sale with your lenders, restore your credit, and help you relocate. Not only will we help you throughout the entire short sale process and offer you all of the services to avoid foreclosure, we will help you to relocate and prepare you to purchase another property within two years

A short sale is when a mortgage lender agrees to and allows a borrower to sell a property for less than the amount that is owed on the mortgage. A short sale is a way to sell your property before your lender finalizes foreclosure proceedings. Most banks prefer to avoid the added expense of foreclosure proceedings, if reasonable third-party buyer purchase offers are presented to the lender.

The negative impact on your credit score is typically less with a short sale than with a foreclosure. In general, after completing the short sale process most lenders will allow you to purchase another property within 2 years. If you are foreclosed on, the lender will report this to the credit bureaus for a period of 7 years. It is also possible to do a short sale and to remain current on your payments. If you are current on your mortgage throughout the short sale process, you can qualify for a loan afterwards without any waiting periods. These options are not available through a foreclosure. Every situation is different, so we recommend that you speak with our preferred real estate attorney who can advise you on the legal and tax implications of a foreclosure and a short sale.

In order to qualify for a short sale, you must show that you are experiencing a financial hardship. Examples of a financial hardship would be a job loss or a reduction in pay, divorce, death of a spouse, illness, medical emergencies, or you are a few payments late on your mortgage and you are having trouble keeping up. Your property must be worth less than the balance of your mortgage in order to qualify.

We do not charge any out-of-pocket expenses to list the property, gather documents and to negotiate the short sale with your lender. If you need legal advice or other services, we have professional affiliates that can help you. Your lender will generally pay for the commission and all closing costs. If you have a second mortgage, the first mortgage lender could require you to pay the discounted second mortgage payoff.

Yes, it is important that you remain in the house during the short sale process as some banks will reject the short sale if the home is vacant.

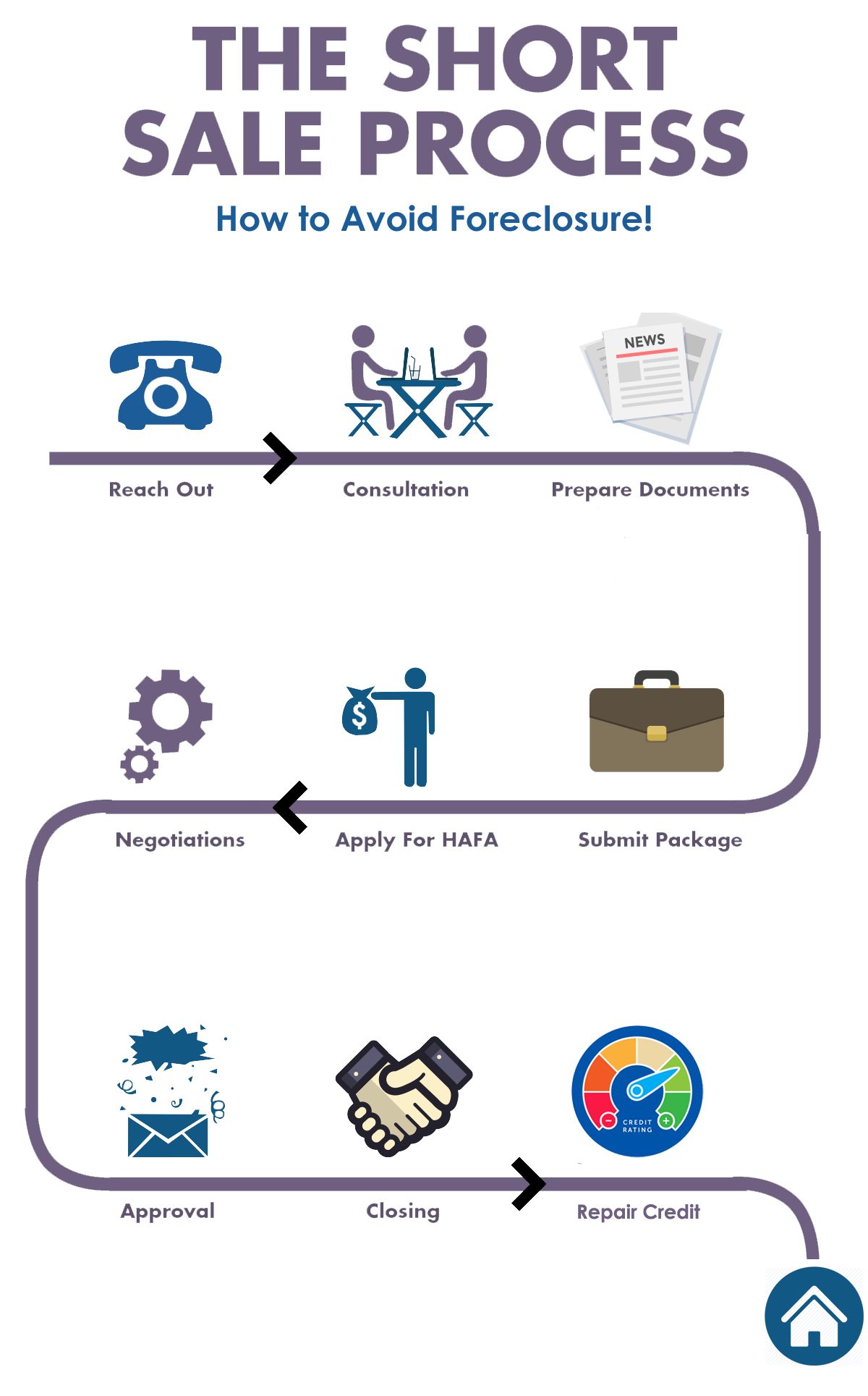

The Home Affordable Foreclosure Program (HAFA) stopped accepting applications in 2017 which provided applicants money for relocation expenses. There are some lenders that offer assistance programs however most lenders do not allow you to receive any money from the sale of your property since the lender is already taking a loss on their loan.

The short sale process can take a few weeks or several months to get an approval. Each lender has different methods of reviewing and in most cases, there are several levels of management, mortgage insurance companies, and investors that will need to review the short sale package. It is important to be patient during the process and for us to follow up often with the lender's assigned negotiator.

Yes. Each mortgage and lien will be negotiated individually. Multiple mortgages from multiple lenders can make the short sale process more complicated and time-consuming as all mortgages and lien holders must agree to a short sale.

Yes, the process is longer and is more complex but we are very experienced in working with homeowners that are in the bankruptcy process.

A Notice of Default is a legal notice document that is recorded at the county recorder's office against the property by the mortgage trustee. This legal document will notify the borrowers that there is a mortgage default and that foreclosure proceedings have been initiated. A copy of this notice will be mailed out to the mortgage defaulting borrowers.

A Notice of Trustee's Sale is a legal notice document that is recorded at the county recorder's office against the property by the mortgage trustee. This legal notice is posted on the property and advertises the location, date and time that the property will be put up for auction.

A lender may offer to release the mortgage against the property in exchange for less than the total amount of the promissory note. A release will allow the property to be sold without paying off the obligations of the promissory note however the note is not satisfied. The advantage of a release is it allows the property to be sold and you avoid a foreclosure. The disadvantage is the remaining debt which is the deficiency still exists. You are still liable for the terms of the promissory note. Most lenders will not pursue the deficiency unless you have other significant assets. If the property goes to foreclosure, you could be liable for deficiencies and the full amount of remaining debt on mortgages beyond your first mortgage. A lender may agree to accept less than it is owed as complete and total satisfaction of the debt and release its lien against the property. Your note and obligation to the lender are satisfied for less than you owe. When the property is sold, the debt is paid off completely. Sometimes short sale negotiations are successful in obtaining complete satisfaction. Sometimes all that can be obtained is a release.

A deficiency judgement is a judgment that is filed against the borrower for the difference between the amount owed on the property and the amount that is paid to the lender. Our goal is to negotiate with your lender for a release of their lien as payment in full without them seeking a deficiency judgment. If the lender decides to pursue a deficiency judgement, we recommend that you speak with our legal representatives.

No, there is no guarantee that the lender will approve a short sale and if the loan is in default the lender will proceed with the foreclosure process. Typically, if the Notice of Trustee's Sale has not been recorded, the lender prefers to accept a short sale rather than foreclose.

Authorization Letter to Release Information – This document authorizes our team to speak and negotiate terms of the short sale with your lender.

Listing Agreement – This is a standard real estate listing agreement that allows us to market your home and the contract terms are subject to lender and property owner approval.

Financials – The lender will request a financial statement, two years of tax returns, 2 most recent bank statements, two years of W-2 or 1099 documents, and 2 recent pay stubs.

Real Estate Purchase Agreement – Buyers will submit offers subject to the lender's approval of the short sale. We will submit offers to the lender for review.

Closing Disclosure– The title company will prepare a closing disclosure that will show the lender the potential lender proceeds after all closing and commission costs.

Negotiator - The lender will assign a negotiator to your short sale file usually within 30 days of the short sale request.

Broker Price Opinion – The lender will order a BPO to determine the current value of your property.

Arm's Length Affidavit – The lender will send an arm's length affidavit that must be signed by the buyer, the seller and the agents.

Approval Letter - The lender will issue a short sale approval letter that will indicate the lender's terms and conditions of the short sale.

If you would like to purchase one of our short sale properties or buy a foreclosure in Utah please provide your contact information and details of what you are looking for and we will alert you when a property is available.